Discovery Library · For Advisors

Decision Risk Is the Most Under-Engineered Retirement Risk — and Social Security Claiming Is Its Purest Form

Decision risk — the risk that a retiree makes an irreversible, value-destroying financial choice — is the only one of the four major retirement risks without a standard planning framework. Social Security claiming is its highest-stakes expression, and it can be engineered.

The Four Risks, and the One Without a Framework

Writing in the Journal of Financial Planning (June 2026), Chris Heye laid out four risks to retirement security: longevity, market, health, and decision risk. Michael Kitces surfaced it in Weekend Reading — which is where we first saw it.

Three of those four already have mature toolkits. Longevity risk has actuarial tables, annuities, and lifetime-income strategies. Market risk has had a framework since Markowitz: modern portfolio theory turned “will the market cooperate?” into an engineering problem with inputs, constraints, and an efficient frontier. Health risk has insurance, HSAs, and long-term-care planning.

Decision risk has none of that. It is named in the literature and acknowledged in client conversations, but it is not operationalized. Advisors are told it exists; they are not handed a repeatable method for reducing it. That gap is the subject of this piece.

Why Claiming Is Decision Risk in Its Purest Form

If decision risk is the danger of getting an irreversible call wrong, Social Security claiming is its cleanest example.

It is one decision, made once, at a single moment. There is no rebalancing, no dollar-cost averaging, no annual review that quietly corrects the drift. You choose a claiming age, benefits begin, and the monthly figure is effectively locked for the rest of your life — and, for the higher earner in a couple, for the surviving spouse’s life too. (A narrow 12-month withdrawal window exists; it rarely rescues a bad decision — see the FAQ below.)

The stakes match the finality. United Income’s 2019 study — The Retirement Solution Hiding in Plain Sight, built on Health and Retirement Study data sponsored by the Social Security Administration — found that only 4% of retirees claim at the financially optimal time. The other 96% leave money on the table, and the sub-optimal decisions cost the average household about $111,000 in lifetime benefits (United Income, 2019).

You cannot dollar-cost-average your way out of a claiming date. That is what makes it a decision-risk problem, not a portfolio problem.

Two Fears Drive Early Claiming. Neither Is a Plan.

Two fears sit behind a lot of early-claiming decisions, and you’ve heard both.

The first is a bet on mortality: ask a client why they’re filing at 62 and you’ll usually hear some version of “I might not live long enough to come out ahead by waiting.” It’s a mortality bet dressed up as a plan — an effectively irreversible, six-figure decision made on a hunch.

The second is insolvency: “It’s going to run out — better grab it while it’s there.” The 2026 Trustees Report, released June 9, gives you the exact counter: the retirement (OASI) trust fund’s reserves are projected to deplete in late 2032, after which incoming payroll taxes still cover about 78% of scheduled benefits. The program doesn’t go to zero. Here’s what the fear misses: that projected shortfall is an across-the-board reduction to scheduled benefits, so claiming at 62 doesn’t exempt a client from it. Early filing buys no protection from insolvency; it just locks in a permanently smaller benefit that’s still exposed to the same future haircut.

Source: SSA, 2026 OASDI Trustees Report (released June 9, 2026).

Both fears are real. Neither is a plan. You already know what should actually drive the decision: break-even age, survivor-benefit coordination, the client’s health and family longevity, earnings record, and the household’s broader income picture. The gap was never your expertise — it’s the tooling to run all of it with the client in the room and turn a gut call into a documented, defensible recommendation. That’s the decision risk MySSAgent is built to close — see how a claiming analysis runs inside your practice.

What Actually Mitigates It: A Framework, Not Intuition

What reduces decision risk is the same thing that tamed market risk: a framework that holds all the variables at once.

A claiming decision is not a single lever. It is the interaction of many: spousal and survivor benefits, full-retirement-age reduction caps, Delayed Retirement Credit accrual, the annual earnings test, COLA mechanics, and the sensitivity of the lifetime result to each candidate claiming age from 62 to 70. No advisor holds all of that in their head simultaneously, and no rule of thumb captures it.

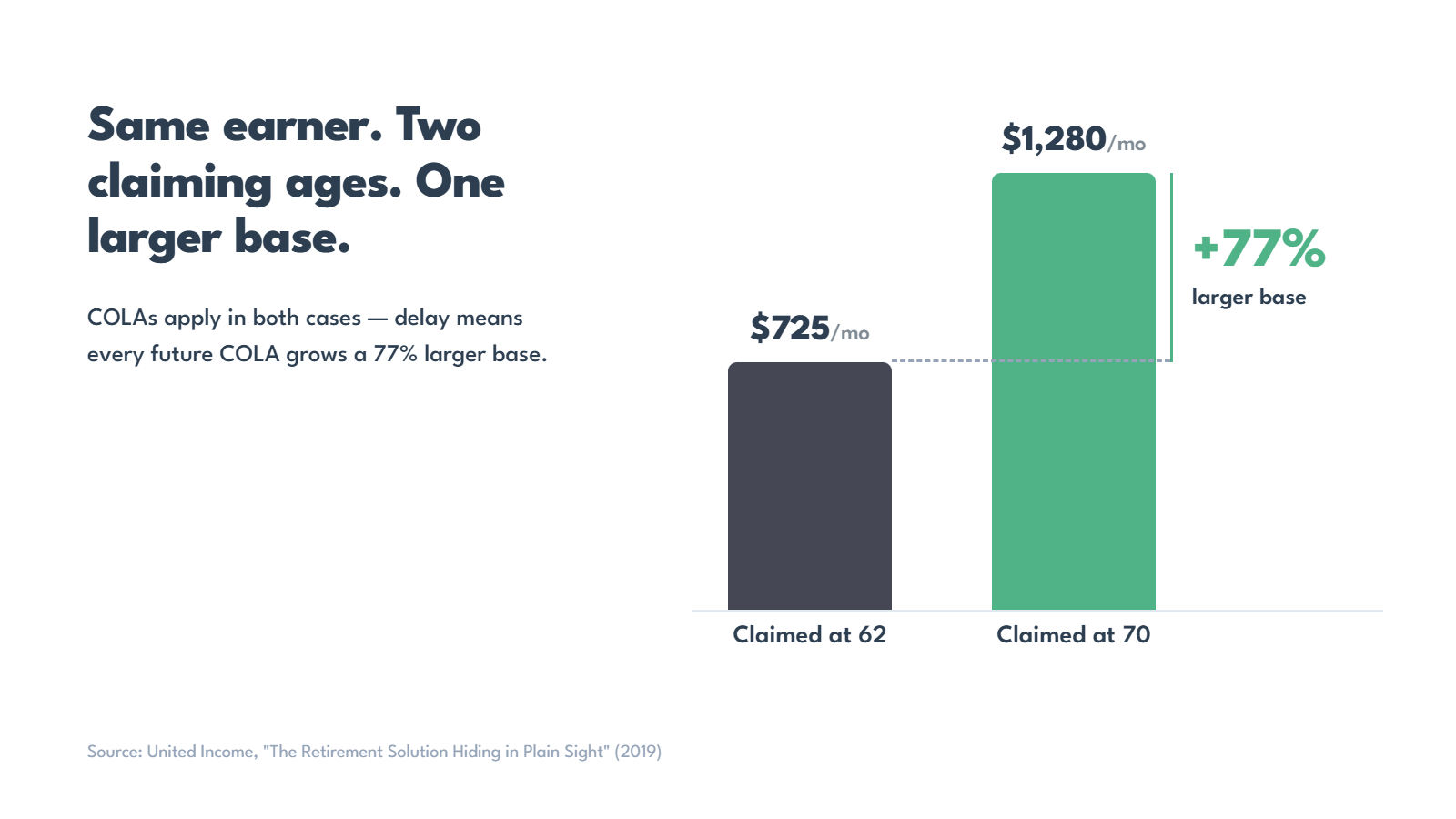

Take just the COLA-and-delay interaction, which is widely misunderstood. COLAs apply to your primary insurance amount every year whether or not you have claimed. Delaying past full retirement age earns Delayed Retirement Credits, which are applied on top of that COLA-adjusted amount — a larger base that future COLAs then grow. It is additive layering, not a single adjustment, and over time the larger base is what separates the two paths.

This is exactly the kind of multi-variable problem software is built for. MySSAgent applies every relevant rule from the 2,728 rules in the SSA handbook to a client’s actual earnings record and household facts, then compares the claiming ages and shows the lifetime-dollar consequence of each — systematically, not by gut. Behind the platform, an RSSA® Credentialed Consultant, Jackie Payne, provides the human verification layer, so the recommended strategy can be both modeled and expert-verified.

The output is not theoretical. In one analysis, the RSSA Roadmap surfaced a $147,000 lifetime gain for a client we’ll call Lorraine, versus the path she was about to take. Individual results vary — but a six-figure swing on a single, irreversible decision is precisely the exposure a framework exists to manage.

Market Risk Had Its Moment. Decision Risk Is at the Threshold.

Market risk stopped being fate and became an engineering problem the day modern portfolio theory gave it a framework. Before Markowitz, “managing” market risk meant judgment and nerve. After, it meant inputs, constraints, and an optimization.

Decision risk is sitting at that same threshold. It is named, it is expensive, and it is still managed mostly by intuition — which is to say, barely managed at all. Claiming is where that gap is most visible and most fixable.

Decision risk doesn’t have an allocation. It needs a framework.