The IRMAA Cliff Your Retirement Plan Ignores

Most retirement plans treat Medicare as a healthcare line item.

That's the first mistake.

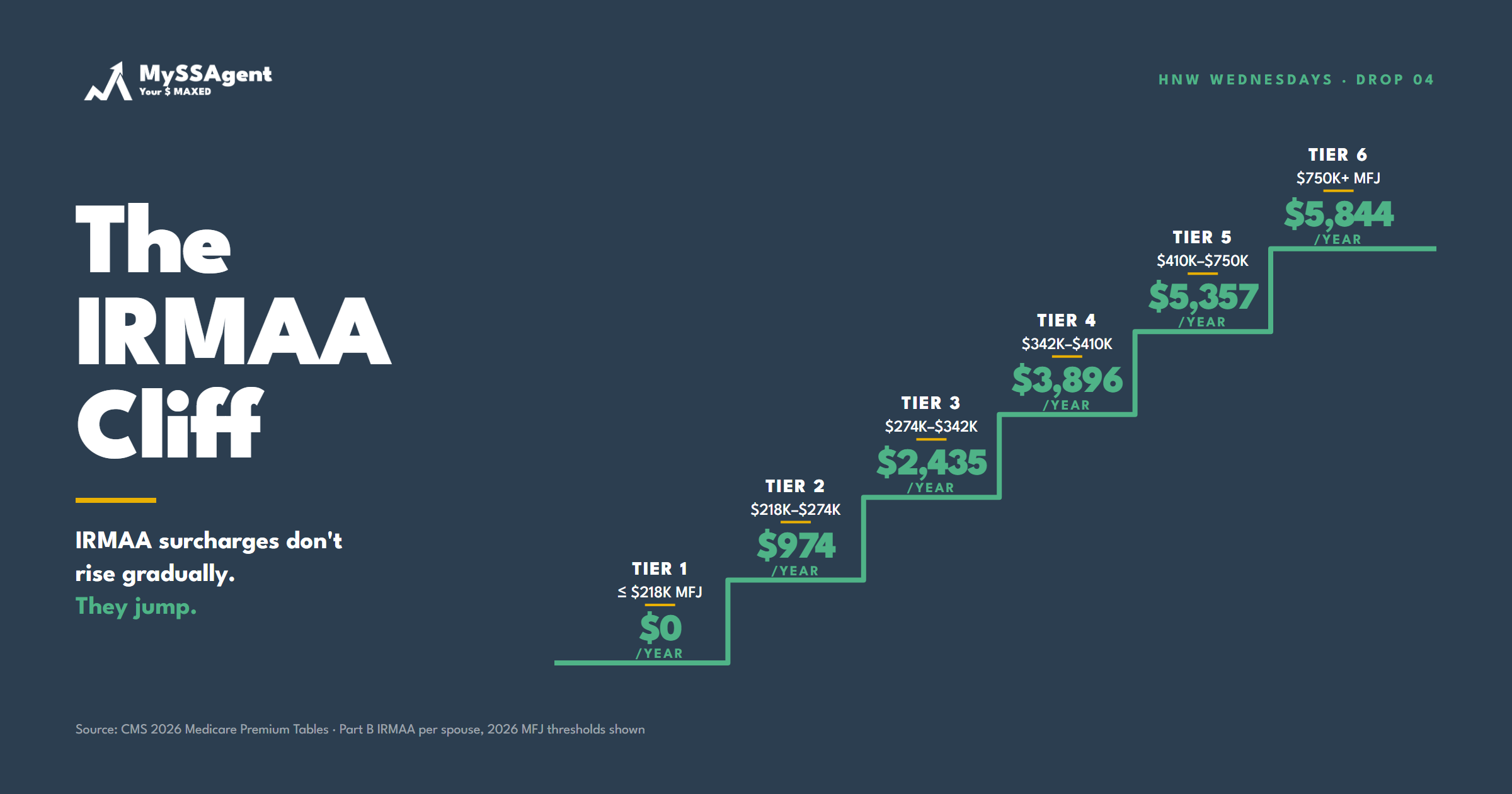

For affluent retirees, Medicare Part B and Part D premiums are an income-driven surcharge structure called IRMAA — Income-Related Monthly Adjustment Amount — and it does not behave like a normal premium. It behaves like a cliff. Cross a threshold by one dollar and the surcharge for the entire year applies. There is no gradual phase-in. The premium just jumps.

And the lookback runs two years.

That last detail is what catches affluent households. The income that determines this year's IRMAA is the MAGI from two tax years ago. Plan a Roth conversion in 2026 without modeling forward, and the cost shows up in 2028 Medicare premiums — for both spouses.

$5,844 per spouse, per year, at the top tier — Part B alone.

Add Part D and the top-tier exposure climbs to roughly $6,936 per spouse, $13,872 for a couple.

That's not a footnote. That's a planning variable.

How the cliff works

The 2026 IRMAA brackets begin at $109,000 MAGI for single filers and $218,000 for joint filers. From there, surcharges scale up across five tiers, capping at $500,000 single / $750,000 joint.

The structure is what matters. IRMAA is not progressive. It is a cliff at every tier boundary.

Cross from Tier 0 ($218,000 joint) to Tier 1 ($218,001 joint) and the household pays an additional $974 per spouse in Part B premiums for the year. Cross from Tier 1 to Tier 2 by one dollar — additional $1,475. The marginal cost of that extra dollar of MAGI is several thousand dollars in Medicare premiums.

Multiply that across two spouses, across both Part B and Part D, and the per-couple stakes get serious.

The two-year lookback

IRMAA in 2026 is determined by 2024 tax returns. IRMAA in 2028 will be determined by 2026 tax returns.

That structural detail breaks a lot of well-intentioned planning.

A client doing a $95,000 Roth conversion in 2026 — a defensible move on its own merits — may push 2026 MAGI just over the next IRMAA threshold. The premium consequence does not arrive in 2026. It arrives in 2028, often after the household has forgotten the conversion happened. The client opens the Medicare premium notice and finds an additional $4,000+ surcharge they did not see coming.

Same problem with one-time events: capital gains realizations, large IRA distributions, business sale proceeds, settlement income. Anything that pushes a single tax year's MAGI over a tier line creates a two-year-delayed Medicare premium surge.

Affluent households tend to have more of these one-time events. They also tend to have higher baseline MAGI, which puts them closer to tier boundaries to begin with.

Where Social Security claiming intersects

The IRMAA cliff is its own planning problem. It is also a Social Security claiming problem.

Claiming Social Security earlier rather than later layers additional taxable income into earlier retirement years. For an affluent household sitting near a tier line, that early benefit can be the difference between Tier 0 and Tier 1 — or between any two adjacent tiers.

Delaying Social Security frees up MAGI room in the early years, which is often when Roth conversions are most valuable. But it also means more taxable income later, when RMDs begin and the household may already be sitting higher in the tier structure.

The right claiming strategy is not the one that minimizes IRMAA in isolation. It is the one that fits cleanly into the household's overall tax-aware withdrawal plan, including IRMAA exposure, conversion timing, and bracket management across retirement years.

That coordination is what separates a Social Security recommendation from a Social Security strategy.

The SSA-44 appeal

One mitigation worth knowing: if the client experienced a qualifying "life-changing event" — most commonly retirement itself — between the lookback year and the premium year, they can file Form SSA-44 to request that more recent income be used.

If the client retired in 2025 and their 2024 tax return reflects a full year of working income, the 2026 IRMAA based on 2024 will be punitively high. SSA-44, supported by 2025 income documentation, can reduce or eliminate it.

Many advisors don't file the appeal because they assume it won't be approved. For legitimate qualifying events, the approval rate is high. The 30 minutes of paperwork can save the client thousands.

The better question

"How do we minimize this client's taxes?" is the wrong question for IRMAA.

The right question is: How do we manage MAGI across the next 5 to 10 years so that no single year's income pushes the household across a tier line we didn't intend to cross?

That question requires modeling Roth conversions, claim timing, withdrawal sequencing, and one-time events together. Not separately. Not after the fact. Together.

It also requires knowing where the tier lines are, where the household sits relative to them, and where the planned distributions will land them in two years.

This is not exotic planning. It is just planning that takes the lookback seriously.

IRMAA doesn't reward optimism. It rewards lookback math.

MySSAgent runs the multi-year MAGI projection alongside claiming strategy — surfacing tier-line crossings before they happen, not two years after.

Advisors: we're opening a founding cohort for firms that want this analysis inside their own practice — early access now. Get founding access →

Professional and Premium analyses include review by a Registered Social Security Analyst® (RSSA®)-credentialed consultant.

RSSA® and Registered Social Security Analyst® are registered trademarks of the National Association of Registered Social Security Analysts, Ltd. (NARSSA).

Source: CMS, "2026 Medicare Parts A & B Premiums and Deductibles." SSA-44 form: ssa.gov/forms/ssa-44.pdf.

HNW Wednesdays — Drop 04 of 8 · A weekly series from Patrice Ayling for affluent households and the advisors who serve them.

Ready to Find Your Optimal Claiming Age?

Run your personalized Social Security analysis in minutes.

Get My Free Analysis