Withdrawal Sequencing, Roth Conversions, and Claiming Are One Decision

Most retirement plans treat withdrawal sequencing, Roth conversions, and Social Security claiming as three separate decisions.

They aren't.

They're one decision, expressed three ways. Treating them separately produces three locally-reasonable answers that combine into a globally-mediocre plan.

That's the problem.

One optimization. Not three.

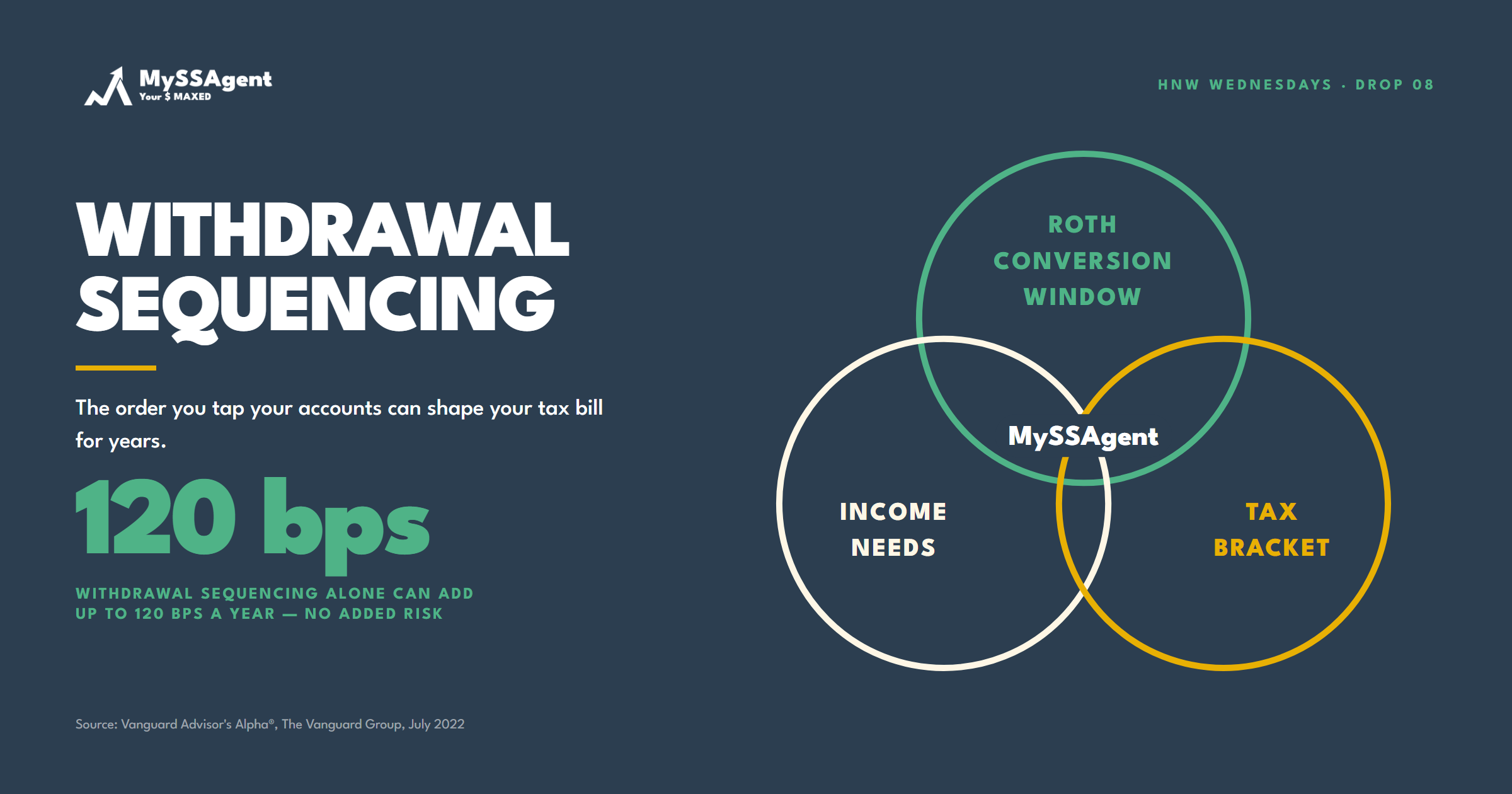

Why these three are actually one

Each of the three decisions changes the same variable: the household's modified adjusted gross income (MAGI) across retirement years.

Withdrawal sequencing — taxable, tax-deferred, tax-free — controls how much taxable income shows up in each year of retirement.

Roth conversion timing controls how much additional taxable income gets layered into specific years to permanently reduce future tax-deferred balances.

Social Security claim timing controls when up to 85% of benefits become taxable household income.

All three move MAGI. All three interact with brackets, IRMAA tiers, and the taxation of Social Security itself. The right amount of any one of them depends on what the other two are doing.

Plan them in sequence — "first decide claiming, then decide conversions, then decide withdrawals" — and each decision gets made with incomplete information.

The Roth conversion window

For affluent retirees, the early retirement years are often the cleanest window the household will ever have for Roth conversions. Working income has stopped. RMDs haven't started. Social Security may not be flowing yet. MAGI is unusually low.

That window is small — typically the gap between retirement age and either RMD age (currently 75 for those born 1960 or later under SECURE 2.0) or Social Security claiming.

Five to ten years of low-MAGI room. Convert too little and the household carries pre-tax balances into the RMD years where conversions become much more expensive. Convert too much and one year's MAGI breaks an IRMAA tier line, costing thousands two years later.

Now layer in claim timing. Claiming Social Security at 67 instead of 70 closes the conversion window three years early. Each of those three years had room for $50,000-$100,000 in conversions at meaningful tax savings. Lost.

Or it didn't. Maybe claiming at 67 was the right call for survivor protection, longevity hedge, or cash flow needs. The point is that the conversion window cost should be priced into the claiming decision, not discovered after the fact.

The provisional income trap

Social Security itself becomes taxable when the household's provisional income — adjusted gross income plus tax-exempt interest plus half of Social Security benefits — exceeds certain thresholds. Up to 85% of benefits can be taxable at the federal level.

Withdrawal sequencing decisions move provisional income directly. A traditional IRA distribution counts in full. A Roth distribution counts not at all. A taxable brokerage withdrawal counts only on the gain portion.

The household withdrawing primarily from traditional accounts pushes more of their Social Security into the taxable column. The household withdrawing primarily from Roth accounts keeps Social Security mostly tax-free.

That difference compounds over a 25-year retirement.

The right sequencing isn't the one that produces the lowest taxable income in any single year. It's the one that produces the lowest cumulative tax across retirement, accounting for how each decision changes provisional income for Social Security taxation purposes.

Bracket management as the unifier

The cleanest way to think about all three decisions together is bracket management.

The household has a target marginal rate it wants to hit each year. For most affluent retirees, that's somewhere between 22% and 24% — high enough to get meaningful Roth conversions done at a defensible rate, low enough to stay below the next bracket break.

Once that target is set, the three decisions collapse into one optimization:

Sequence withdrawals to land MAGI in the target bracket.

Convert enough to fill the remaining bracket headroom each year.

Time Social Security to maintain bracket discipline across the years it begins to flow.

That's not three decisions. That's one decision with three levers.

Modeled separately, each lever moves to a locally-optimal position that interferes with the others. Modeled together, they coordinate.

Why this gets handled poorly

Most planning software handles each decision in its own module. The Social Security analyzer is one workflow. The Roth conversion calculator is another. The withdrawal sequencing tool is a third. The advisor runs each, accepts each output, and assumes the combination is roughly optimal.

It usually isn't.

Three locally-optimal answers built from independent assumptions tend to overlap, conflict, or leave bracket headroom on the table. The household ends up with claiming timing that ignores the conversion window, conversions that ignore the IRMAA cliff, and withdrawals that ignore Social Security taxation.

Each decision is defensible. The combination is mediocre.

Specialist Social Security planning — the kind that integrates with bracket management and conversion windows rather than running in parallel — produces a different output. The Social Security claim timing becomes one of three coordinated decisions, not a standalone recommendation.

The advisor's output stops being three answers and starts being one plan.

The better question

"What's the optimal Social Security claiming age for this client?" is the wrong question to lead with.

The better question is: What sequence of withdrawals, conversions, and claim timing keeps this household at the target marginal rate across all 25 years of retirement?

That question integrates three decisions into one. It accepts that the right Social Security age depends on the conversion plan and the withdrawal plan, not the other way around.

It also produces better answers.

Three decisions handled separately produce three correct answers and one mediocre plan. One decision handled together produces a strategy.

MySSAgent runs the integrated optimization — claim timing, withdrawal sequencing, and Roth conversion windows together — at the household level, against actual brackets and IRMAA tier lines.

Advisors: we're opening a founding cohort for firms that want this analysis inside their own practice — early access now. Get founding access →

Professional and Premium analyses include review by a Registered Social Security Analyst® (RSSA®)-credentialed consultant.

RSSA® and Registered Social Security Analyst® are registered trademarks of the National Association of Registered Social Security Analysts, Ltd. (NARSSA).

Source: SSA + IRS provisional income rules. SECURE 2.0 RMD age: 75 for those born 1960 or later.

HNW Wednesdays — Drop 08 of 8 · A weekly series from Patrice Ayling for affluent households and the advisors who serve them.

Ready to Find Your Optimal Claiming Age?

Run your personalized Social Security analysis in minutes.

Get My Free Analysis