Zero Years Are Quietly Shrinking Your Business Owner's Benefit

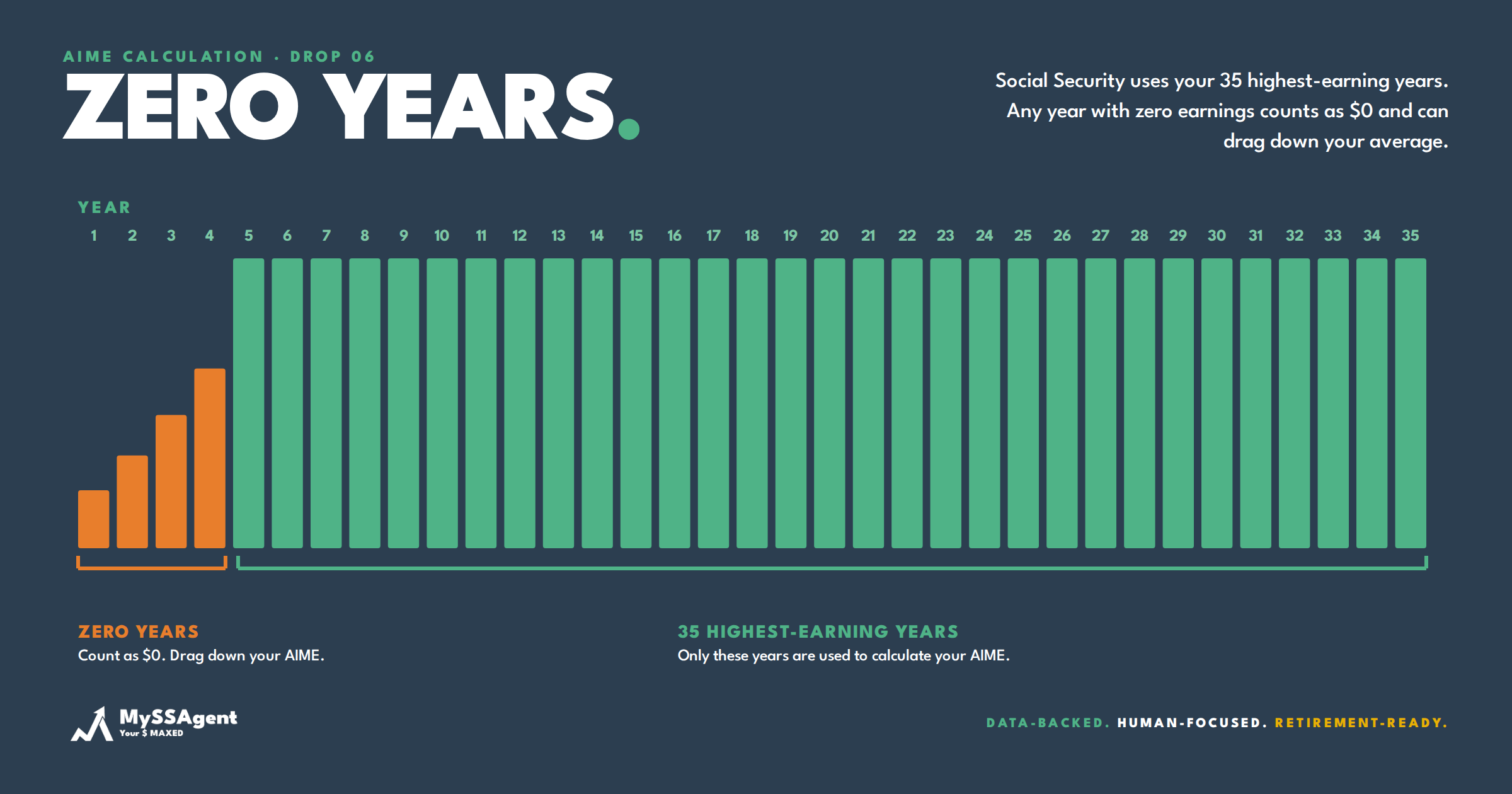

Social Security calculates a worker's primary insurance amount (PIA) by averaging their highest 35 years of indexed earnings.

Years 36 and beyond don't count. Years missing from the record count as zero.

For a salaried W-2 worker with 40+ continuous earning years, this is invisible. The 35 highest are the ones the system uses, the rest are noise. The PIA reflects a clean career.

For a business owner, it can be a real problem.

35.

That's the number of years that build the AIME (Average Indexed Monthly Earnings), which becomes the PIA, which becomes the monthly benefit.

Any year with $0 in covered earnings averages in as a $0.

Five zero years in the record will pull the AIME down measurably. Ten zero years will pull it down a lot.

How business owners create zero years on purpose

A successful business owner often has a tax strategy that minimizes W-2 income and maximizes pass-through distributions. Reasonable wage, the rest as profit distribution. The math works for income tax purposes — distributions don't carry payroll tax — and the cash flow looks the same.

It does not look the same to Social Security.

Distributions don't go into the earnings record. Only W-2 wages and self-employment income subject to SE tax do.

The owner who spent ten years drawing $40,000 in salary and the rest in distributions has ten years of $40,000 in their earnings record — not the $200,000+ they actually earned.

Push that further. The owner who spent five years drawing zero salary because the business reinvested everything has five zero years.

Zero years aren't a paperwork issue. They are real entries in the earnings record that pull the AIME calculation down.

The fix needs lead time

The fix is simple in concept and underused in practice.

Three to five years of intentional wage planning before claiming.

If the owner is 60 and intends to claim at 67, they have seven years to materially reshape the AIME calculation. Bumping W-2 wage to the Social Security maximum ($184,500 in 2026) for those years replaces the lowest-indexed years in the 35-year window. If those low years were zeros, the swap is dramatic.

If the owner is 63 and planning to claim at 67, they have four years. Less leverage but still meaningful — particularly if the existing record has multiple zero years.

If the owner has already claimed, the window is closed. The PIA is set.

This is one of the few Social Security planning levers that requires action before retirement, not at retirement.

The trade-off

Higher W-2 wage means higher payroll tax — 6.2% employee, 6.2% employer (12.4% combined for self-employed) — on amounts that previously came through as distributions.

For a maximum-earner business owner adding $144,500 of W-2 wage in place of distribution, that's roughly $17,900 in additional payroll tax for the year. Spread over 3-5 years, the total cost is $54,000 to $90,000.

Whether that's worth it depends on what the resulting PIA increase is worth in lifetime benefits — including survivor benefit reinforcement.

For a high-earner couple where the business owner is the higher earner and the surviving spouse will rely on the larger benefit, the lifetime present value of a meaningful PIA increase often exceeds the payroll tax cost. For a household where the business owner's PIA matters less to the survivor planning, the math may be tighter.

The point is that the trade-off can be modeled. It usually isn't.

What this requires from the planning team

This problem sits at the intersection of CPA-side compensation strategy and advisor-side claiming strategy. It requires both.

The CPA needs to know that the tax-optimal compensation structure during the building years has a Social Security cost, and that the cost compounds for life if not corrected before claiming.

The advisor needs to know that the client's earnings record may not reflect the client's actual earning power, and that the gap is fixable with lead time.

When those two conversations don't happen — or happen separately, without coordination — the business-owner client arrives at retirement with a PIA that's quietly smaller than it should be.

Smaller benefit. Smaller survivor benefit. Smaller COLA-adjusted lifetime income.

The fix isn't expensive. The cost of skipping it is.

The better question

"What's this client's projected benefit?" is the wrong question for business owners.

The better question is: What does this client's earnings record actually look like, and where are the years that are dragging the AIME down?

Pull the earnings record. Look at the numbers. If there are zeros or low years inside the 35-year window, the conversation is whether to fix them — and how much lead time exists to do it.

That conversation is the planning value.

Distributions optimized the tax bill. Wages build the benefit. Both decisions deserve a seat at the table.

MySSAgent pulls the earnings record, identifies the zero/low years inside the AIME window, and models the lifetime impact of intentional wage planning across the runway to claiming. Insight from Jeff Firestone, CPA.

Advisors: we're opening a founding cohort for firms that want this analysis inside their own practice — early access now. Get founding access →

Professional and Premium analyses include review by a Registered Social Security Analyst® (RSSA®)-credentialed consultant.

RSSA® and Registered Social Security Analyst® are registered trademarks of the National Association of Registered Social Security Analysts, Ltd. (NARSSA).

Source: SSA earnings record + AIME formula. 2026 Social Security wage base: $184,500. Insight from Jeff Firestone, CPA.

HNW Wednesdays — Drop 06 of 8 · A weekly series from Patrice Ayling for affluent households and the advisors who serve them.

Ready to Find Your Optimal Claiming Age?

Run your personalized Social Security analysis in minutes.

Get My Free Analysis